BRRRR strategy mistakes usually happen when investors treat one profitable projection as a finished deal. The BRRRR method depends on five connected steps: buy, rehab, rent, refinance, and repeat. If one step fails, the next step becomes harder, more expensive, or impossible.

- What Is the BRRRR Strategy?

- Why BRRRR Deals Fail: The Compounding Risk Problem

- Mistake #1: Overestimating After Repair Value (ARV)

- Mistake #2: Underestimating Carrying Costs

- Mistake #3: Buying in the Wrong Market or Neighborhood

- Mistake #4: Working With the Wrong Contractor or No Contract

- Mistake #5: Ignoring Refinance Lender Requirements

- Mistake #6: Taking on a Project Too Big for Your Experience

- Mistake #7: Incomplete or Over-Rehab

- Mistake #8: Misjudging Time to Rent and Time to Refinance

- Case Study: How One Investor Lost $27,000 on a Single BRRRR

- What to Do When the Appraisal Comes in Low

- Who Should and Shouldn’t Use the BRRRR Strategy?

- FAQs About BRRRR Strategy Mistakes

- What is After Repair Value (ARV) and how do I calculate it?

- How long is the seasoning period before I can refinance?

- Can I pull 100% of my cash out on a BRRRR refinance?

- How much should I budget for carrying costs during rehab?

- What is the difference between a hard money loan and a DSCR loan?

- Is BRRRR still viable in a high-interest-rate environment?

- Can BRRRR work with vacation rentals or short-term rentals?

- Final Thoughts: The BRRRR Strategy Works Only When the Math Survives Reality

A strong BRRRR deal is not just a cheap house with a big after repair value (ARV). It is an investment property that can survive rehab delays, carrying costs, lender rules, tenant placement, appraisal pressure, and refinance limits. New investors often lose money because they underestimate how each risk compounds. A missed rehab budget hurts cash flow. A low appraisal traps capital. A delayed refinance keeps expensive money in the deal longer than expected. The goal of this guide is to show the most common BRRRR strategy mistakes, why they kill deals, and how investors can fix them before closing.

What Is the BRRRR Strategy?

The BRRRR strategy is a real estate investing method where an investor buys a distressed or underperforming property, rehabs it, rents it to tenants, refinances based on improved value, and repeats the process with recovered capital. BRRRR is an acronym for Buy, Rehab, Rent, Refinance, Repeat.

The appeal is simple: the investor aims to recycle the same cash into multiple rental property deals. Instead of selling after rehab like a flip, the investor keeps the asset and uses a cash-out refinance to recover part or all of the original money.

The basic BRRRR method looks like this:

- Buy: Purchase below market value.

- Rehab: Improve the property and force appreciation.

- Rent: Place qualified tenants and prove rental income.

- Refinance: Replace short-term financing with long-term debt.

- Repeat: Use recovered capital for the next deal.

The strategy works when the numbers are conservative and the execution is clean. It fails when investors assume every step will go perfectly.

Why BRRRR Deals Fail: The Compounding Risk Problem

BRRRR deals fail because the strategy stacks several risks in sequence. The investor must buy right, complete the rehab, rent quickly, hit the expected ARV, qualify for the refinance, and keep enough cash flow after debt service.

A normal rental purchase has risk. A BRRRR deal adds construction risk, appraisal risk, financing risk, and timing risk. One mistake can create pressure across the entire project.

For example, if rehab costs go $15,000 over budget, the deal may still look fine on paper. But if the property also takes two extra months to rent and the appraisal comes in $20,000 low, the investor may not recover enough money to repeat.

The BRRRR risk chain looks like this:

| Step | Main Risk | Deal Impact |

|---|---|---|

| Buy | Paying too much | Lower equity spread |

| Rehab | Budget overruns | More cash trapped |

| Rent | Vacancy delay | Less rental income |

| Refinance | Low appraisal or lender denial | Capital stays stuck |

| Repeat | No recovered funds | Portfolio growth stops |

This is why the BRRRR strategy rewards disciplined underwriting more than optimism.

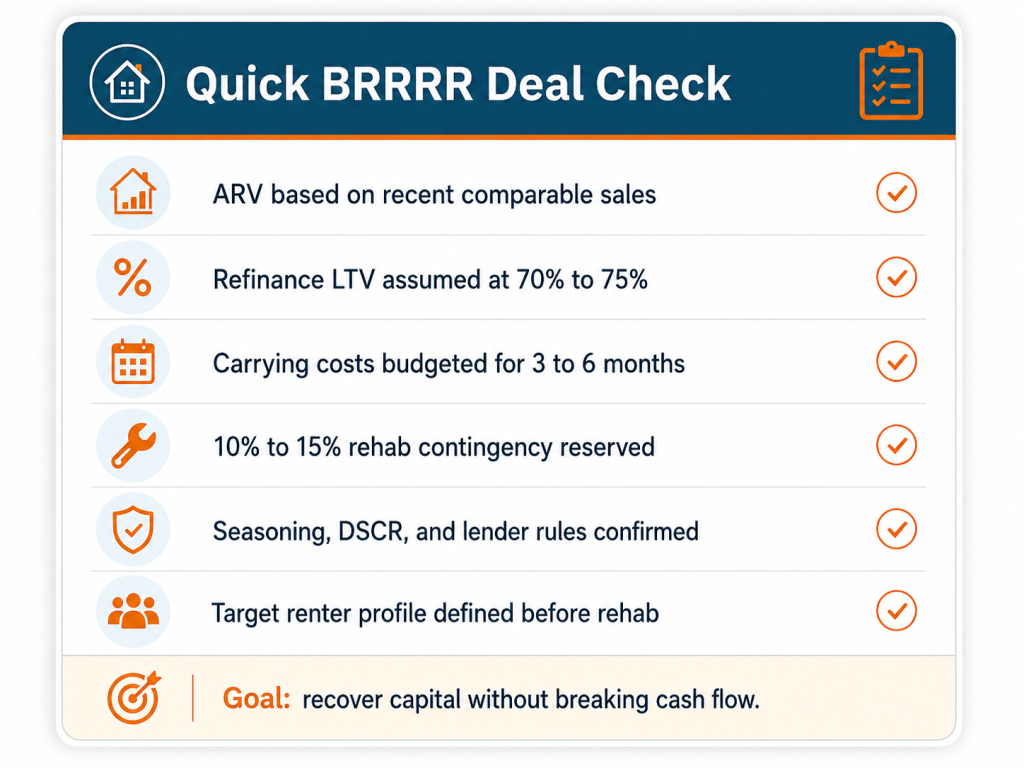

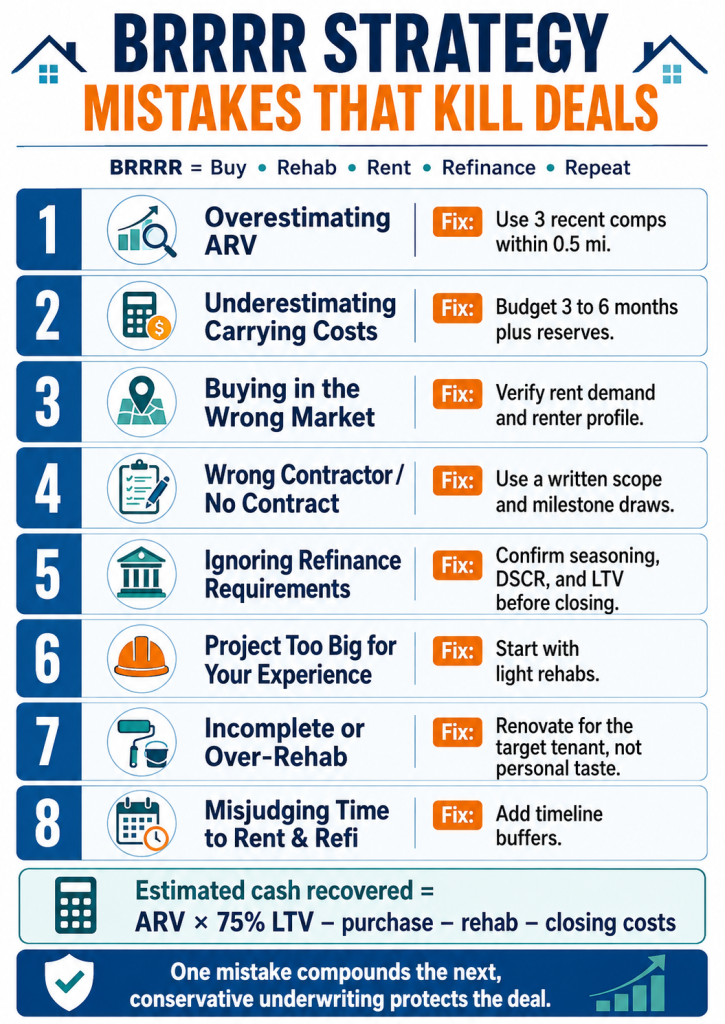

Mistake #1: Overestimating After Repair Value (ARV)

Overestimating after repair value (ARV) is the most dangerous BRRRR mistake because the refinance depends on the finished property’s appraised value. If the ARV is wrong, the investor may not pull enough money out to repay the loan, recover rehab costs, or repeat the strategy.

What it looks like:

The investor assumes the property will appraise like the best house in the neighborhood, even though the property is smaller, on a weaker street, or finished with lower-quality materials.

Why it kills deals:

Most cash-out refinance loans are capped by loan-to-value (LTV). If a lender allows 75% LTV and the appraiser values the property at $200,000, the maximum loan is about $150,000 before closing costs and lender adjustments. If the appraisal comes in at $170,000, the refinance may only support about $127,500.

The basic recovery formula is:

ARV × refinance LTV minus purchase price minus rehab costs minus closing costs = estimated cash recovered

The fix:

Use conservative comps. Pull at least three comparable sales within 0.5 miles and the last 90 to 180 days where possible. Match property type, square footage, bedroom count, condition, parking, and school district.

Red flag checklist:

- The ARV depends on one perfect comp.

- The comp is across a major road or in a better school zone.

- The real estate agent or wholesaler gives an ARV with no supporting comparables.

Mistake #2: Underestimating Carrying Costs

Underestimating carrying costs turns a profitable BRRRR deal into a break-even or negative deal. Carrying costs are the expenses paid while the property is being rehabbed, rented, and refinanced.

What it looks like:

The investor budgets the purchase and rehab but forgets interest, taxes, insurance, utilities, lawn care, snow removal, permits, loan extensions, and vacancy.

Why it kills deals:

Carrying costs eat the spread between the purchase price and the refinance. This is especially painful when using a hard money loan, private money loan, bridge loan, or other short-term financing with higher interest.

Common carrying costs include:

| Cost | Why It Matters |

|---|---|

| Loan interest | Paid before refinance |

| Property taxes | Continue during rehab |

| Insurance | Often higher on vacant properties |

| Utilities | Needed for work and inspections |

| Maintenance | Exterior upkeep during vacancy |

| Loan extension fees | Triggered by project delays |

The fix:

Budget carrying costs for at least three to six months, even if the rehab looks quick. Add a reserve equal to 10% to 15% of the rehab budget for scope creep.

Red flag checklist:

- The deal only works if the rehab finishes in 30 days.

- No budget exists for utilities or insurance.

- The investor has no cash reserve after closing.

Mistake #3: Buying in the Wrong Market or Neighborhood

Buying in the wrong market kills BRRRR deals because the property must attract tenants, support the ARV, and qualify for stable long-term financing. A cheap property is not automatically a good investment property.

What it looks like:

The investor buys a low-priced house without checking rental demand, crime patterns, job access, school zones, tenant quality, property management availability, or resale activity.

Why it kills deals:

The rent step supports the refinance. Lenders often review rental income, market rent, DSCR, and property condition. If the neighborhood cannot attract reliable tenants, the deal may fail even after a successful rehab.

A weak market can create:

- Longer vacancy during rent-up

- Lower rental income than projected

- Higher maintenance and turnover

- Lower appraisal support

- Lower buyer and lender confidence

The fix:

Underwrite the neighborhood before the property. Confirm rent comps, days on market, tenant demand, property manager feedback, and recent sales activity. A property manager can often tell you faster than a spreadsheet whether a renter profile matches the house.

Red flag checklist:

- The only attraction is a low purchase price.

- Rental comps are old or far away.

- Local property management companies avoid the area.

Mistake #4: Working With the Wrong Contractor or No Contract

Working with the wrong contractor can destroy a BRRRR project through delays, poor workmanship, change orders, and unfinished rehab work. The general contractor controls one of the most expensive parts of the strategy.

What it looks like:

The investor hires the cheapest contractor, starts work without a written scope, pays too much upfront, or fails to define payment milestones.

Why it kills deals:

Contractor delays increase carrying costs. Poor work can fail inspection. Scope creep can consume the investor’s capital before the property is ready to rent or refinance.

The fix:

Use a written contract with a detailed rehab scope, payment schedule, deadline, material standards, permit responsibility, and change order process. Pay based on completed milestones, not promises.

A basic contractor control system includes:

- Written scope of work

- Itemized rehab budget

- Start and finish dates

- Proof of license and insurance where required

- Draw schedule tied to completion

- Photo updates and site walkthroughs

Red flag checklist:

- The contractor refuses written pricing.

- The contractor asks for most of the money upfront.

- The bid is far below every other estimate.

Mistake #5: Ignoring Refinance Lender Requirements

Ignoring refinance lender requirements is a common BRRRR mistake because investors often focus on the purchase and rehab while assuming the refinance will be easy. The refinance is the step that determines whether capital comes back or stays trapped.

What it looks like:

The investor buys with hard money, completes the rehab, places a tenant, and only then learns that the lender has seasoning, LTV, DSCR, DTI, title, or appraisal requirements that the deal does not meet.

Why it kills deals:

A refinance lender may cap loan-to-value, require a seasoning period, verify rental income, review debt-to-income (DTI), or use a debt service coverage ratio (DSCR). Fannie Mae’s cash-out refinance guidance includes a title seasoning requirement where at least one borrower generally must have been on title for at least six months before the new loan disbursement, with listed exceptions.

The fix:

Talk to the lender or mortgage broker before closing on the purchase. Ask about seasoning, LTV, DSCR loan options, conventional cash-out refinance rules, appraisal rules, reserves, credit score, and entity ownership.

Key lender questions are listed below:

| Question | Why It Matters |

|---|---|

| What LTV applies to this property type? | Determines cash recovered |

| Is there a seasoning period? | Controls refi timing |

| Is DSCR allowed? | Helps when DTI fails |

| Are LLC-owned properties eligible? | Affects title structure |

| What rent documentation is required? | Supports income |

Red flag checklist:

- No refinance quote before purchase.

- The investor assumes 100% cash recovery.

- The property is bought in an entity the lender will not accept.

Mistake #6: Taking on a Project Too Big for Your Experience

Taking on a project too big for your experience increases execution risk. BRRRR investing rewards skill, but new investors often confuse a large discount with a good deal.

What it looks like:

A beginner buys a property needing foundation work, major plumbing, electrical upgrades, roof replacement, permitting, fire damage repair, or commercial conversion without the team or capital to manage it.

Why it kills deals:

Complex projects have more unknowns. Big rehab work increases the chance of delays, failed inspections, contractor disputes, and cost overruns. It can also extend the seasoning period and delay rental income.

The fix:

Match the project to your skill level. New investors usually do better with cosmetic or light value-add rental property projects before moving into heavy rehabs.

A beginner-friendly BRRRR project often has:

- Functional roof and structure

- No major foundation issues

- Clear rental demand

- Simple cosmetic rehab

- Predictable permit needs

- Multiple exit options

Red flag checklist:

- The property has structural issues.

- The rehab budget is larger than the purchase price.

- The investor has never managed a similar project.

Mistake #7: Incomplete or Over-Rehab

Incomplete rehab and over-rehab both hurt BRRRR results. Incomplete rehab lowers rent and appraisal quality. Over-rehab traps money in upgrades the renter profile will not pay for.

What it looks like:

The investor either cuts corners on important repairs or installs luxury finishes in a workforce rental neighborhood.

Why it kills deals:

The appraiser and tenant both react to the finished product. A poor rehab may reduce the appraised value. An excessive rehab may look nice but fail to increase rental income or ARV enough to justify the cost.

The fix:

Rehab for the renter profile and the refinance, not personal taste. In a standard residential BRRRR, durable flooring, clean paint, safe systems, working appliances, and functional kitchens and bathrooms usually matter more than luxury finishes.

Red flag checklist:

- The scope is not tied to rent comps.

- The investor chooses finishes based on personal preference.

- Major safety or system repairs are delayed to save cash.

Mistake #8: Misjudging Time to Rent and Time to Refinance

Misjudging time to rent and time to refinance creates pressure after rehab. The property may be finished, but the investor still needs a tenant, lease, appraisal, underwriting, and loan closing.

What it looks like:

The investor assumes the property will rent in a week and refinance immediately after the tenant moves in.

Why it kills deals:

Vacancy during rent-up reduces cash flow. Refinance delays keep expensive short-term money in place. Interest rate increases between purchase and refinance can also reduce the final loan amount or weaken cash flow.

The fix:

Build the timeline backward. Confirm the lender’s seasoning period, required lease documents, appraisal timeline, rent verification, and underwriting process before the rehab is complete.

A realistic timeline includes:

| Stage | Planning Range |

|---|---|

| Rehab completion | Depends on scope |

| Rent-up | 2 to 8 weeks in many markets |

| Refinance application | After lender documents are ready |

| Appraisal and underwriting | Several weeks |

| Seasoning period | Commonly 3 to 12 months depending on loan type and lender |

Red flag checklist:

- No leasing plan before rehab ends.

- No property manager selected.

- Refinance timing is based on hope, not lender rules.

Case Study: How One Investor Lost $27,000 on a Single BRRRR

A real BRRRR failure often comes from several small misses happening together. Business Insider reported on an investor whose BRRRR project ended up about $27,000 in the hole after rising costs, a lower-than-expected value outcome, and financing pressure affected the plan.

Here is a simplified version of how a similar deal breaks:

| Item | Projection | Actual |

|---|---|---|

| Purchase price | $95,000 | $95,000 |

| Rehab budget | $35,000 | $52,000 |

| Expected ARV | $180,000 | $155,000 |

| 75% refinance value | $135,000 | $116,250 |

| Carrying costs | Lower estimate | About $6,500 |

| Result | Capital recycled | About $27,000 trapped |

The lesson is not that BRRRR never works. The lesson is that BRRRR does not forgive thin margins. A lower appraisal, contractor delay, and carrying costs can erase the entire plan.

What the investor should do differently:

- Use more conservative ARV comps.

- Add a rehab contingency.

- Confirm refinance terms before buying.

- Budget holding costs for delays.

- Keep enough capital to survive a failed refinance.

What to Do When the Appraisal Comes in Low

A low appraisal does not always kill a BRRRR deal, but it does change the exit plan. The investor must decide whether to challenge the value, refinance less cash out, hold longer, or restructure financing.

The first step is to review the appraisal for weak comps or errors. If the appraiser used outdated sales, different property types, or ignored completed improvements, the investor may submit a reconsideration of value with better comps.

Practical options include:

- Dispute the appraisal with stronger comparables.

- Request a second appraisal if the lender allows it.

- Refinance partially and leave some capital in the deal.

- Hold longer until more comparable sales support the value.

- Negotiate seller credits before purchase on future deals.

- Use a DSCR loan if income supports the debt better than personal DTI.

A low appraisal is painful, but the worst response is pretending the original ARV is still real.

Who Should and Shouldn’t Use the BRRRR Strategy?

The BRRRR strategy is best suited for investors who understand rental underwriting, rehab management, financing, and property operations. It is not ideal for someone who wants passive investing from day one.

BRRRR may fit investors who:

- Have cash reserves

- Understand rehab costs

- Can manage contractors

- Know local rental markets

- Have lender relationships

- Want to build a long-term portfolio

BRRRR may not fit investors who:

- Need all cash back immediately

- Have no emergency capital

- Cannot handle construction risk

- Do not understand lender requirements

- Want completely passive income

- Are uncomfortable with vacancy and repairs

Commercial BRRRR, vacation rentals, and short-term rental strategies can work, but they require different underwriting. Cap rate, seasonality, operating expenses, zoning, and management intensity become more important.

FAQs About BRRRR Strategy Mistakes

What is After Repair Value (ARV) and how do I calculate it?

After Repair Value (ARV) is the estimated value of a property after the rehab is complete. Investors calculate ARV by comparing the finished property to similar recently sold properties nearby. Good comps should match location, size, condition, bed and bath count, and property type.

How long is the seasoning period before I can refinance?

The seasoning period before a refinance commonly ranges from 3 to 12 months depending on the lender, loan type, title structure, and refinance program. Conventional cash-out refinance rules and DSCR loan programs may treat seasoning differently, so investors should confirm requirements before buying.

Can I pull 100% of my cash out on a BRRRR refinance?

No, investors cannot assume they will pull 100% of their cash out. Most refinance loans use LTV caps, often around 70% to 75% for investment property cash-out scenarios, depending on the lender and program. Closing costs, appraisal value, and loan limits also reduce cash recovered.

How much should I budget for carrying costs during rehab?

Investors should budget carrying costs for the full expected rehab, rent-up, and refinance timeline, plus a delay buffer. A practical starting point is three to six months of interest, taxes, insurance, utilities, maintenance, and loan fees.

What is the difference between a hard money loan and a DSCR loan?

A hard money loan is usually short-term financing used to buy and rehab a property. A DSCR loan is commonly used as long-term rental property financing where the lender focuses on whether rental income covers the debt payment. Hard money often funds the project. DSCR often supports the refinance.

Is BRRRR still viable in a high-interest-rate environment?

Yes, BRRRR can still work in a high-interest-rate environment, but the margin for error is smaller. Higher rates reduce cash flow, lower refinance proceeds, and make DSCR qualification harder. Conservative ARV, lower purchase price, and stronger rental income become more important.

Can BRRRR work with vacation rentals or short-term rentals?

Yes, BRRRR can work with vacation rentals, but the risk profile is different. Short-term rentals depend on seasonality, local regulations, furnishing costs, platform demand, cleaning systems, and higher property management intensity. Investors should not underwrite a vacation rental like a standard long-term rental.

Final Thoughts: The BRRRR Strategy Works Only When the Math Survives Reality

The biggest BRRRR strategy mistakes come from optimistic assumptions. New investors often assume the rehab will finish on time, the property will rent immediately, the appraisal will hit the target ARV, and the refinance will return all their cash. Real deals rarely move that cleanly.

A better BRRRR strategy starts with pressure testing. What happens if the rehab costs 15% more? What happens if the appraisal is 10% low? What happens if the property sits vacant for two months? What happens if the lender caps the LTV lower than expected?

The BRRRR method remains a powerful real estate investing strategy when investors buy conservatively, control rehab risk, verify lender rules, match the renter profile, and keep enough money in reserve. The goal is not just to close a deal. The goal is to finish with a stable rental property, healthy cash flow, and enough recovered capital to repeat without forcing the next mistake.